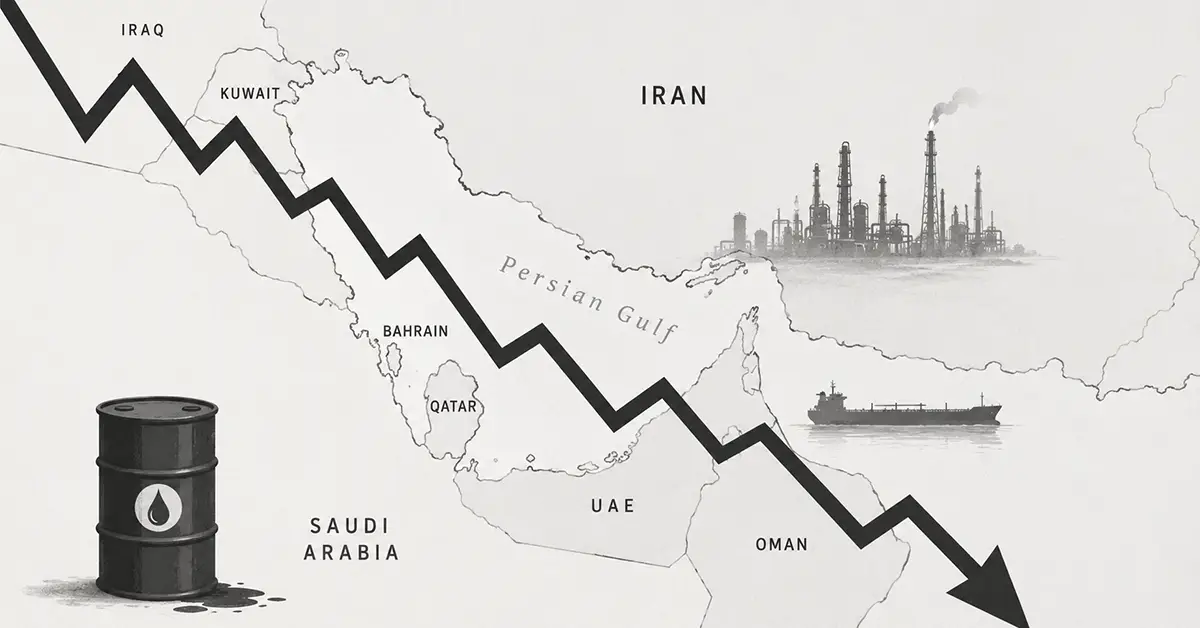

When Donald Trump and Benjamin Netanyahu launched Operation Epic Fury on 28 February, they had ‘a very simple message’: Iran ‘will never have a nuclear weapon’. After the first two weeks of devastating bombing, oil prices spiking and markets falling, Trump has gone back and forth, changing the timelines, claiming victory (‘total and complete victory – 100%’ on 9 April) before making new threats. Yet the Iranian regime remains in place and the Strait of Hormuz closed – the narrow chokepoint through which a fifth of the world’s petroleum products normally pass.

On 4 May the US compounded this with its own blockade of Iranian ports, ‘Project Freedom’, promising to escort ships through the strait. Two days later Trump declared the operation over but threatened more bombing ‘at a much higher level and intensity than it was before’ if Iran does not accept his deal – which, making no concessions to the regime, it is unlikely to do.

The USA cannot retreat, but after two months it has not beaten Iran. All of Trump’s bluster, boasts and renewed threats are simply compounding the economic uncertainty, with no end in sight. The global economic consequences continue to mount.

On 20 March the International Energy Agency (IEA) released a report assessing the scale, likely duration and possible mitigations of the crisis. Its conclusion was unambiguous. The fallout from this war will create the ‘worst fuel shock in history’, larger than 1973, 1979 and 2022 combined, removing more than twice as much oil from global circulation as the 1970s crises did at their peak.

IEA member nations have approved the release of 400 million barrels from emergency reserves, the largest such release in history. It is a measure of how seriously the world’s energy institutions are treating this crisis that they have reached immediately for their most extreme tool. But as the IEA itself acknowledges, strategic stock releases offer only temporary relief. They cannot resolve an ongoing supply disruption with no end in sight.

Inter-imperialist tensions

US strategy in the Middle East can be understood through the prism of inter-imperialist competition. Israel functions as a regional gendarme, the guarantor of US interests in this strategic region. Iran represents the principal challenger, with deep economic links to China and India through its oil exports. It has been a member of BRICS since 2024, an emerging alternative economic bloc around China, organised in competition with the US-led blocs and institutions.

Although China has diversified its domestic energy supply and has a large uptake of electric vehicles among its population, it remains the world’s largest oil and liquefied natural gas (LNG) importer. China’s economy is reliant on the Strait of Hormuz, with over one-third of its oil supply – 5.4 million barrels per day – passing through it.

Given China’s reliance on export-led growth, reduced global demand will compound the damage. A sustained blockade does not just harm Iran; it also harms China, as Trump is well aware. But a conflict that damages Chinese economic interests on this scale carries a risk of even deeper tensions between the world’s two largest powers.

The main beneficiary of the war so far appears to be Russia. Moscow benefits directly from sustained high oil prices, which it can now demand thanks to the US relaxing sanctions on its exports, and has every interest in seeing the US bogged down in a prolonged and costly military confrontation while it continues its grinding invasion of Ukraine.

Comparisons to the Iraq War of 2003 are instructive. Then the US was able to assemble a coalition of willing partners and operate with at least the tacit acceptance of its major allies. Today Trump’s aggressive diplomatic posture towards Europe has left the US and Israel essentially isolated. EU states are bearing the economic consequences of a war they were not consulted on and cannot influence – a situation that is deepening the transatlantic fracture Trump has spent years widening.

But Iran is not Iraq. It has spent two decades preparing for exactly this confrontation, developing decentralised military and nuclear infrastructure specifically designed to survive the kind of shock-and-awe campaign now being deployed against it. Iran’s demonstrated ability to withstand US military pressure is undermining American standing as the world’s dominant power.

Having declared mission accomplished, the US cannot now retreat without a severe loss of credibility. Meanwhile the blockade is hitting the economies of China and US allies alike, the world economy and ultimately the USA’s own, where support for the war is already splitting Trump’s MAGA base.

System on the brink

If you were to judge the economic impact of this war purely from US stock markets, you might conclude that the effects were minimal. Markets are at an all-time high. But this picture is profoundly misleading.

The apparent health of the global economy is less a reflection of real productive growth than the product of frenzied investment in artificial intelligence in the US. Vast sums of capital are being poured into AI infrastructure, data centres and technology stocks in anticipation of returns that have not yet materialised and may never do so at the scale being priced in. This has all the hallmarks of a classic speculative bubble, and is acutely vulnerable to external shocks.

A sharp, sustained rise in energy costs puts enormous pressure on the construction and logistics sectors, including the firms contracted to build the AI data centres on which current market valuations depend. If those building programmes falter, confidence in AI sector valuations could collapse, and with it a significant portion of the financial architecture holding up global markets.

Alongside and intertwined with the AI bubble sits a ballooning private credit market. Since 2008, shadow banking in the form of private credit has expanded dramatically. Unlike conventional bank lending, private credit is largely unregulated, highly leveraged and illiquid. This war did not arrive in a period of capitalist stability. It arrived precisely when the system’s capacity to absorb a major shock is severely degraded. If central banks respond to war-driven inflation by raising interest rates, they risk triggering a debt crisis in the private credit market directly.

Shortages

The most immediate economic consequence of the war is a severe disruption to global energy and commodity supply chains. Brent crude, the global benchmark, has recently hit highs of $126 per barrel, matching the peaks reached at the outset of Russia’s invasion of Ukraine in 2022. Iran’s military command has warned the world to ‘prepare for $200 per barrel’.

The scale of the shock is laid bare in the World Bank’s April 2026 Commodity Market Outlook. The Energy Price Index rose 41.6% in March. European natural gas increased by 59.4%, exceeding even the 55.7% spike recorded at the height of the 2022 energy crisis, while Brent crude jumped 45.8% by the end of March. Although prices have dropped somewhat as markets reacted to Trump’s announcement of ‘Project Freedom’, they remain around $100 per barrel and will rise sharply again if a settlement is not reached quickly.

But crude oil is only part of the picture. Refined petroleum products such as diesel and kerosene are even more significantly affected, with direct consequences for transport, agriculture and heating. LNG prices, already elevated as a result of the Ukraine war, are rising rapidly, pushing up household heating costs across the global north.

The conflict has already removed approximately 19 to 20% of the world’s near-term LNG supply. Some countries in the global south have already been forced into desperate measures. Kenya, for instance, has weakened its fuel sulphur standard for six months, raising the permitted limit from 10 to 50 parts per million in an attempt to offset supply shortages—a short-term fix with serious long-term consequences for public health, engine infrastructure and air quality.

Less discussed but equally significant are the petrochemical by-products on which the global economy depends. Iran is a major producer of urea and ammonium nitrate, the fertilisers on which modern industrial agriculture relies. The strait also carries vast quantities of helium, a critical input in semiconductor manufacture and other industrial processes.

Maritime insurance costs have compounded all of this further. Before the war, risk premiums were roughly 0.05% to 0.2% of a vessel’s hull value. Following the first air strikes, these rose to between 1.5% and 3%. Vessels with connections to the US, UK or Israel – referred to in shipping circles as ‘missile magnets’ – have seen rates climb as high as 5% to 7.5%. For a standard oil tanker valued at $100 million, a single seven-day trip through the Gulf that previously cost around $200,000 in insurance now costs approximately $5 million to $7.5 million. This cost is passed on to every consumer at the end of the supply chain.

Stagflation

Fossil fuels underpin all production and transport in the modern economy, so price rises here create a broad swell of inflation. Their by-products inject another round of cost hikes across whole sectors such as agriculture, where food prices hit workers and the poor hardest; and further inputs to industry – plant oils, biofuels, raw materials like cotton – add a third layer of costs.

Workers are already feeling the effects of this crisis at the petrol pump and in the supermarket, but the true economic consequences are still to be felt. The knock-on effects of the blockaded strait will drive up prices and scarcities across the whole global economy and could well push it into recession. Inflation of this nature cannot be managed simply by raising interest rates – and, as noted above, an attempt to do so risks detonating the overstretched private credit market.

For workers in Britain and across Europe, this is not a fresh crisis arriving in a period of stability. The cost-of-living crisis that began in 2022 with the Ukraine war was never fully resolved. Real wages in Britain remain below their 2008 peak across many sectors. Had wages grown at their pre-2008 trend, workers would be approximately £10,000 to £14,000 better off per year.

Food prices are already 50% higher than in 2021. Many homes are heated with natural gas or oil, both hit very hard by the blockade and the destruction of production facilities across the Gulf. When winter arrives this will become a severe and immediate problem for many millions. The working class is being asked to absorb a second major energy shock without having recovered from the first.

The macroeconomic picture for Britain is bleak. GDP growth has been anaemic: 0.3% in 2023, 1.1% in 2024 and an estimated 1.4% in 2025. The OECD has already revised its UK growth forecast for 2026 down from 1.3% to 0.8% as a direct result of the conflict. Forecasts predicting UK inflation to average 3.2% this year seem optimistic. The IMF has warned that in a possible global recession the UK would be the worst hit of the world’s advanced economies.

Stagnant growth combined with rising inflation is known as stagflation, a crisis particularly devastating for the working class because it combines falling real wages and rising unemployment with rising prices. This would mark the second such crisis in Britain in four years.

Meanwhile big oil companies around the world are predicted to make immense super-profits if the price of a barrel stays at $100 or over. British companies are leading the way. Shell has already announced over £5 billion in profits for the first quarter and BP £3.8 billion – both more than double last year’s – as they profiteer out of the crisis at consumers’ expense.

Global food crisis

The food crisis is perhaps the starkest expression of how war abroad translates into rising prices at home and hunger on a catastrophic scale in the global south. Food prices are already rising as fuel costs feed through to agriculture and distribution.

In the global north the form the crisis takes will be different but no less real: sustained food price inflation hitting a working class whose food bank usage, rent burden and debt levels already reflect years of declining living standards. In Britain, the Food and Drink Federation has warned that food inflation could dwarf its earlier forecast of 3.2% and hit 10% by the end of the year. In large parts of the semi-colonial world, the food crisis will be catastrophic.

The disruption to fertiliser supply has fallen at the worst possible moment, the sowing season. The Fertiliser Price Index rose by 26.2% in March, driven almost entirely by a 53.7% surge in urea prices. Many farmers are choosing not to plant this season at all, as the cost of fertiliser now outstrips any return they could expect from selling their crop. Input shortages mean that for whatever does get planted, the harvest will be reduced.

This is compounded by a further development that has received insufficient attention: China’s decision to halt fertiliser exports has cut off the primary alternative source of supply for much of South Asia. The consequences are particularly severe for rice cultivation – the staple crop for billions across the region, and one that depends heavily on nitrogen-based fertilisers. Multiple countries face disrupted harvests simultaneously, with no alternative supply available at any price.

This is not happening in a vacuum. The Ukraine war produced a severe wheat and sunflower oil crisis in 2022 that drove food prices to record levels globally. Food systems have not recovered from that shock. This is the second major supply disruption in four years, hitting a global agricultural economy already under severe pressure from the climate crisis and the long-term decline of rural incomes. Commodity speculation will accelerate the process further, with financial markets pricing in scarcity before it materialises, generating price rises independently of any actual physical shortage.

The worst of the crisis will be felt most acutely in sub-Saharan Africa, South Asia and across the Middle East itself – the regions most dependent on food imports, most exposed to fertiliser price rises and least able to absorb the shock. Sudan imported 54% of its fertilisers by sea from the Gulf region in 2024, followed by Sri Lanka, Tanzania and Somalia at 36%, 31% and 30% respectively.

Yemen faces catastrophic deterioration. Afghanistan relies on Iran for 30% of its key imports, with prices of cooking oil and some vegetables already surging by 13% in the past month. Nine million Afghan children – one in three – face severe hunger.

Many countries across Asia and Africa are already in famine conditions as a direct result of years of war, in which the US, the European powers and the Gulf states have been deeply complicit. A series of civil wars, insurgencies and land wars – often treated by the media in the north simply as ‘Islamist’ terror – have left millions vulnerable to starvation.

The World Food Programme has estimated that an additional 45 million people will be pushed into acute hunger as a result of this war, reaching a record high of 363 million, with roughly two-thirds in Africa. The result will be food riots and revolts.

Cost of living

The cumulative effect on British workers will be that, by autumn, most households will be significantly worse off, with many already feeling the pinch after years of low wage growth and rising prices. Funds that should be going towards raising wages, rebuilding the NHS and solving the housing crisis are instead being poured into rearmament. We need a united front of the working class and the oppressed to resist the inevitable attempts to make us pay for a crisis we did not create.

Such a united front would draw together socialist organisations, workers striking against falling real pay, community organisations and, crucially, the latent mass power of the trade unions. They could draw up an emergency programme to protect workers from the crisis.

It should demand: a sliding scale of wages and benefits indexed to real prices, as determined by workers’ price-watch committees – grassroots bodies that monitor and publicise real price rises independently of official indices; free public transport to reduce dependence on fuel; a price cap on energy costs; rent controls to protect those already pushed to the edge by the housing crisis; and an increase to welfare spending, not defence spending.

Socialists support punitive taxes to seize the super-profits of the energy profiteers, but to solve the energy crisis as well as climate change the whole sector should be nationalised without compensation, under workers’ and users’ control, and reoriented to renewables.

The united front also needs to be international. As the imperialist powers seek to offload the worst of the crisis onto the slenderest shoulders of the semi-colonial world, we need to extend solidarity by fighting to stop arms exports to warzones, to cancel the crippling debts, and to support all strikes and uprisings against the effects of the crisis. That is the real meaning of ‘globalise the intifada’.

This is not just an economic struggle; it is a political struggle against the imperialism that causes such wars in the first place. Socialists can use the struggles against war and the food crisis to build a new revolutionary workers’ International, able to coordinate struggles across the globe against the capitalist system. To rid the world of war, poverty, hunger and inequality for good, we will have to overthrow it.